Back when there used to be plays and musicals on Broadway and elsewhere, one of my favorites was “Wicked”, which is the fun musical that is the “preqel” to The Wizard of Oz. One of the bring-down-the-house numbers in Wicked is titled “Popular”, in which Glinda, the Good Witch, tries to get Elphaba, the future Wicked Witch of the West, to accept and become what is popular. Good song; funny song, but to no avail as it turns out. When I watched a recent piece about what are called Meme Stocks, I made a mental connection with Wicked, and though I’m not from Boston, I see Meme Stocks as “wicked popular”. Perhaps this is a good connection in an artistic sense, but are Meme Stocks a good investment for you? In my opinion, no financial advisor worth their fees could in their right mind recommend that someone invest a substantial sum in Meme Stocks. Yet, part of the piece I saw (which aired on a “wicked popular” financial news network) described how companies are now trying to figure out how to become Meme Stocks. Why is that? Because Meme Stocks tend to go up and become unhitched from their fundamentals, which is all good for the management of Meme Stock companies.

What are Meme Stocks?

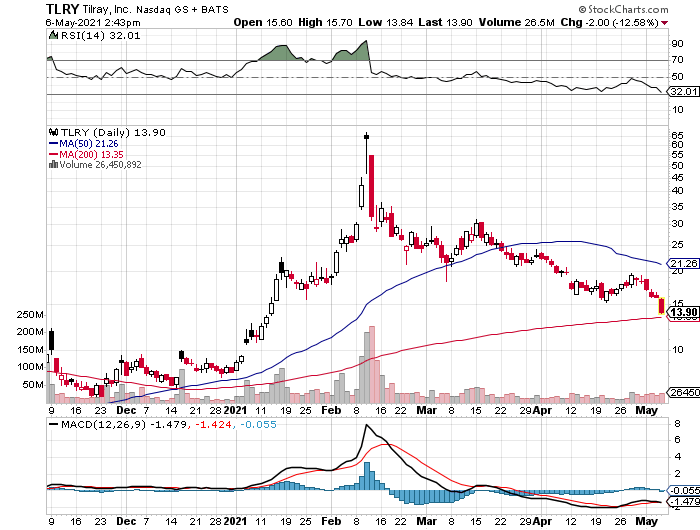

“Meme Stocks” is the term used to describe stocks that get caught up in discussions on Reddit, Stock Twits, or other social media forums and get substantially bought up by retail investors as a result. Gamestop was an early example of this phenomenon, followed by others such as AMC Entertainment, Bed Bath and Beyond (?!), and perhaps Tesla and Blackberry. Each of these has seen a significant upturn in ownership by retail investors, abetted by commission-free trading on platforms such as Robinhood, in addition to the Reddit discussion, which may or may not be a form of collusion. Combatants in the Meme Stock battle buy positions because they believe they are “sticking it to the man”; the man being perhaps a hedge fund, bank, or an otherwise wealthy character of despicable reputation who may have a short position in the stock. The hottest, most wicked popular meme stock right now is AMC, which owns movie theaters. AMC’s CEO, Adam Aron, has become a mini-celebrity as well as very wealthy as a result of the stock’s run-up this year. Good for him, but I think his good fortune has been a result of luck much more than skill.

Should You Play?

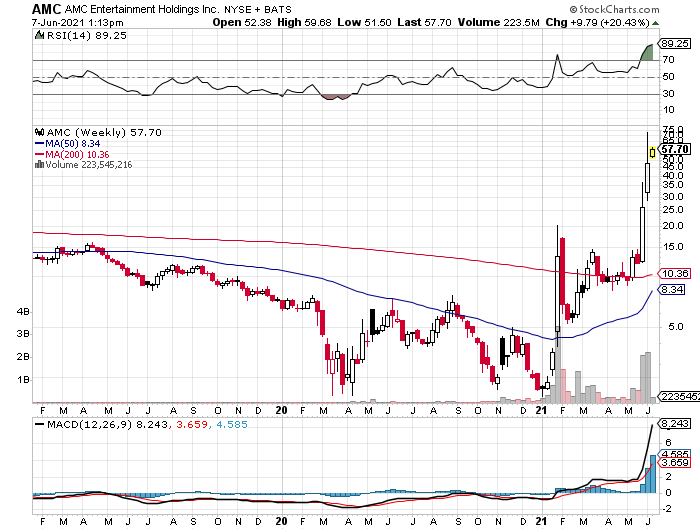

Let’s take AMC as an example. Before the Pandemic, AMC was a sleepy stock trading in the $10-range, and subject to significant headwinds. AMC needs people to go out to its theaters to make money, and even before the pandemic, this was becoming more troublesome because of aging demographics, alternative options for watching movies (think Netflix or other streaming services), and crappy offerings by the Hollywood studios. Not a great business model in my opinion, and investors agreed as AMC stock to stay above $10. Then the pandemic hit, forcing the complete closure of AMC theaters, which are struggling to reopen to this day. At the start of this year, AMC traded in the $2-range. Things looked bleak. Then, sometime in late January, AMC became wicked popular in chat rooms, and retail investors started to buy. AMC’s float was pretty weak (i.e., it was thinly-traded), and this played into the hands of the chat roomers. Now AMC is at $56. I ask you: Do you think the headwinds I described above are better or worse from AMC’s standpoint now that we are emerging from the pandemic as opposed to prior to the start of the pandemic? I’ll use the Socratic method here to give you my answer. Has our population gotten older or younger on balance as the pandemic has raged? (Sadly, perhaps it has gotten somewhat younger, but for the wrong reasons, as Covid deaths have been disproportionately among our elders). Do you think potential movie-goers are more or less inclined to go out and watch a film in the theater now with all of the other streaming options available? And do you think the shutdown of filming as a result of Covid will cause more or fewer movies to be produced? In short, I see AMC’s headwinds as much worse now. So what possible justification can I find to buy AMC at $56 when I didn’t like it at $10 or $2? Corporate reorganization aside, AMC is not an asset-rich company, and don’t see AMC being worth $56 under any scenario.

IMO

When a stock becomes a wicked popular Meme Stock, be very skeptical. True, retail investors can take advantage of a short or a low-float situation and cause a run-up in a thinly-traded stock. However, retail investors are fickle, and their attention spans can be quickly altered when the next great opportunity emerges. Though it is a growing segment, only a very small percentage of investors participate in chat rooms, and while their power may seem large when confined to a single stock, it is not broad enough to sustain any fundamental change in a company. Unless you really have money and time to waste, don’t play in the wicked popular Meme Stock carnival.