Not really – you can refinance at any time if you aren’t looking for the lowest possible mortgage rate. However, mortgage rates are up and there is better chance they will continue to rise than fall over the next year, as all longer-term interest rates are projected to rise. So, if you haven’t yet refinanced and taken advantage of low mortgage rates, now is the time to do it.

Mortgage Bankers Association

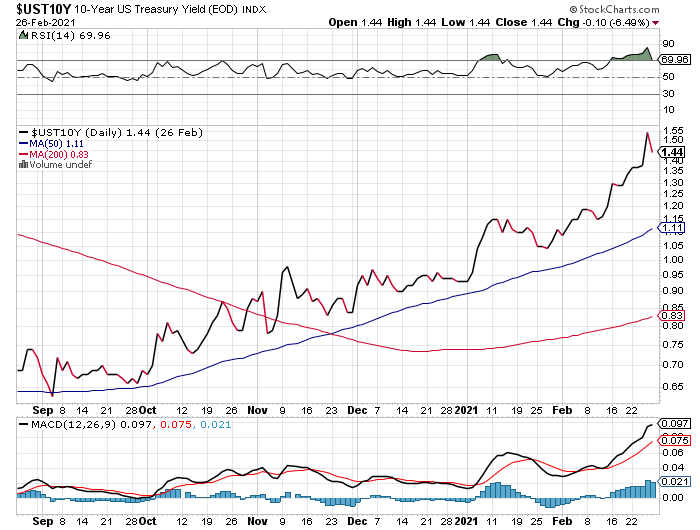

According to this article from Calculated Risk, the Mortgage Bankers Association (MBA)’s Weekly Survey from last week shows that average 30 Year Fixed rates have risen 50 basis points since the beginning of this year and now average 3.36%. Not bad, but not as appealing as the sub-3% rates we saw during Q4 2020. As a result, the article goes on, their “refinance index” is down 5% from the prior week’s survey, meaning that fewer applications for refinance are being submitted. This doesn’t mean the housing market is weak. On the contrary, it is significantly stronger and is expected to remain so due to, as the article says, inadequate housing inventory.

Human Nature

If you think about it, it makes sense that refinances will decline as mortgage rates go up. As with any purchase decision – and I consider a mortgage refinance to be a purchase decision because the borrower likely doesn’t need to refinance – if the price is going down, the buyer/borrower will wait to see if the price might go down some more before committing to the transaction. This is called bottom-fishing, and it is also indicative of why deflation is such a bad economic thing: people refrain from economic activity if the price is going down. Then, once rates bottom out or even rise a bit, borrowers will put their chips on the table and commit. They will continue to refinance as rates go up slightly – I am speaking in a macro sense here – until it no longer makes economic sense to refinance. This could take a long time if the borrower hasn’t refinanced in a while, or it could be a short time for serial refinancers.

Pros and Cons of Refinancing

The obvious pro of refinancing is that you have a lower interest rate and a lower monthly payment, especially if you don’t take any “cash out” in the process of your refinance. Another pro is that you might be able to pull some cash out if your home has appreciated significantly since your prior loan and you need a lump sum of money for some reason. Some families finance their children’s college educations through cash-out refinances, which is a very good way to do it because it is better to pay for college by borrowing in the low-3%’s and paying it back over 30 years than it is to borrow at the higher rates of some student loan programs.

The cons of refinancing include the following:

- You may have to pay points and/or fees for your refinance loan, which means comparing your current mortgage rate to the new proposed mortgage rate is not an apples-to-apples comparison. You have to factor in the cost of these fees and points, which the lender should provide to you when it quotes you the Annual Percentage Rate (APR) of the new loan.

- One of the reasons your monthly payment goes down is because, with the new mortgage, you now have a new 30 year timetable for paying off your loan. Let’s say you were 10 years into your prior loan: that means you would have your house paid off in 20 years at the current payment. Now, although you are paying less per month with the new loan, you won’t pay off your house for another 30 years. Of course, you can always make extra principal payments that will speed up the payoff process – typically with no penalty payable to the lender. Or you can refinance into a 15 year fixed rate loan, and get the lower rate (and potentially lower payment) and still own your home free and clear in 15 years.

- If you take cash out as part of a refinance, now you owe more. No problem, you may say, as long as your loan is 80% loan-to-value or lower, meaning that you have at least a 20% equity cushion if you have to sell your house. And, you may be right if you feel like you are in a growing area with a strong housing market. However, don’t take the decision lightly if you are considering a cash-out refinance. It could get you into a financial bind down the road.

IMO

I believe you should act now if you are considering a mortgage refinance if you want a good rate. I believe mortgage rates will rise over the next year, so don’t wait. With the for-sale housing market as strong as it is, there is a better possibility that your house will appraise out at a value that will justify the loan amount that you want, especially if you are looking to take cash out of the transaction.