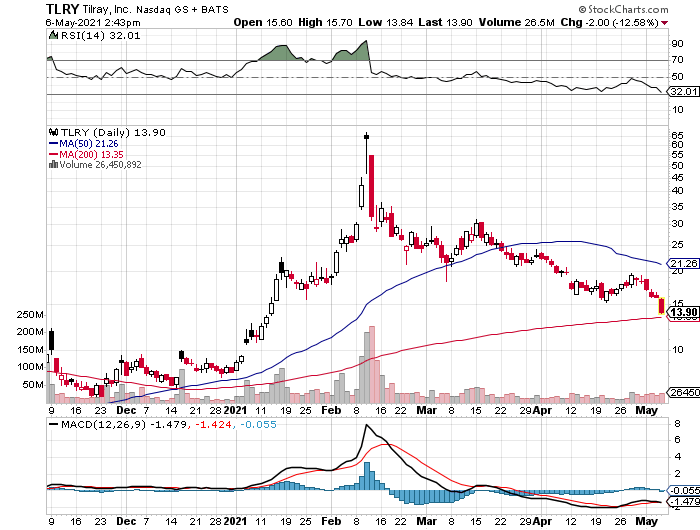

Tilray gets a lot of press because of the industry it plays in: Cannabis. i.e. Marajuana. Tilray’s mission is “to build the world’s most trusted and valued cannabis and hemp company.” Fair enough. It is getting more press this week because its merger with Aphria, another cannabis seller, closed, wherein the former CEO of Aphria (Irwin Simon) became the CEO of the combined company, which will continue to be known as Tilray. Despite all of this press, Canada-based Tilray has continued to lose boatloads of money. Although cannabis legalization is moving forward in the USA (it is already legal in Canada), I believe Tilray faces a steep uphill battle to reach profitability. I would not invest in Tilray stock, nor of the stock of most any other cannabis stock. Read on to see why I believe so.

Losses

Check out Tilray’s most recent 10K for 2020. The report is long on the future prospects of cannabis and therefore on the company, as well as on the risks of being in this business. However, the financial results are not a highlight. You have to scroll all the way to Page 64 of the report to find a summary of their financial results. Page 64 shows a gross profit of $24.7 million on sales of $210.5 million (gross margin of 11.7%). Good enough, but Tilray’s combined selling, general and administrative expenses (sg&a) totaled $140.5 million, or 67% of gross sales. Then Tilray shows a write-off of $61 million, which is 29% of gross sales, for “impairment of assets”. Cannabis is an organic product that can go bad. Tough way to do business. My take is that this is a low-margin business with product that easily can go bad in the warehouse, and that sg&a expenses are extraordinarily high for the company’s sales. Said another way, Tilray’s gross sales will have to increase enormously in order to justify what they are spending now for sg&a, let alone what they would be spending in sg&a if their sales were to increase. I don’t see Tilray reaching profitability any time soon, even with the merger with Aphria (Aphria’s financials are not part of Tilray’s 2020 10K).

Low Barriers to Entry

My fundamental problem with investing in Tilray or any other publicly-traded cannabis company is that the barriers to entry into the cannabis business are low, and that the hardcore cannabis users are already invested in the “alternative” growers and suppliers, or they just grow their own. Anyone can grow their own marijuana in their own backyard or even in a pot in their apartment. Just acquire some seeds from a buddy and off you go. In fact, growing one’s own is a primary aspiration of many hardcore users. My sense is that the Tilray’s of the world will attract new cannabis users, at least for a while. I believe the appeal of growing one’s own is part of the allure of cannabis, and this points to the issue of low barriers to entry in the cannabis industry. It is hard to establish a footing when literally anyone can get into the business of growing marijuana.

Demand Overstated

Despite the new applications for cannabis – CBD creams, oils, gummies, and the like – I believe the demand for cannabis and its derivative products will prove to be overstated. I have tried CBD cream on various body aches (hey, it’s legal), and it does work, but not substantially more than non-CBD topical products such as Emu oil or traditional Ben Gay, all of which I have also tried. Moreover, CBD creams are much more expensive. I believe people will try CBD creams just to check it out, but given its relative cost, I don’t believe sales will be sustainable. Yes, there will always be the traditional market for consumption of cannabis, but with its health benefits are clearly debatable at best, I don’t view its sales growth as something we should promote. In short, I don’t see cannabis demand exploding to the extent Tilray needs it to in order to become consistently profitable.

Health Benefits

The current advocates of cannabis products tout its health benefits. I agree that my CBD cream seems to work on my body aches. However, the problem is that all of these claims are word of mouth. Traditionally, if you have a substance or a chemical that you believe has health benefits, you test it with lab animals, then apply to the FDA to test it with humans, and then go through the FDA process to get the substance approved so you can sell it with the substantiated claims of health benefits. The problem is that cannabis is so widely available that it can’t be patented, and if it can’t be patented, a company such as Tilray cannot take it through the FDA approval process. As such, the health benefits of cannabis will always have to be word of mouth. Tilray will never be able to mark up the price of its cannabis because it doesn’t have an exclusive, patent-protected right to sell it or its health benefits. Consequently, the cannabis business will remain a relatively low-margin business, which will keep it a hard business to make money in.

IMO

As you can tell, I am not a proponent of Tilray or of any player in the cannabis business. The industry is a low-margin business with too may barriers to entry, with demand and health benefits I believe to be overstated. Tilray specifically has a bloated level of overhead that I don’t foresee it growing out of. Stay away.