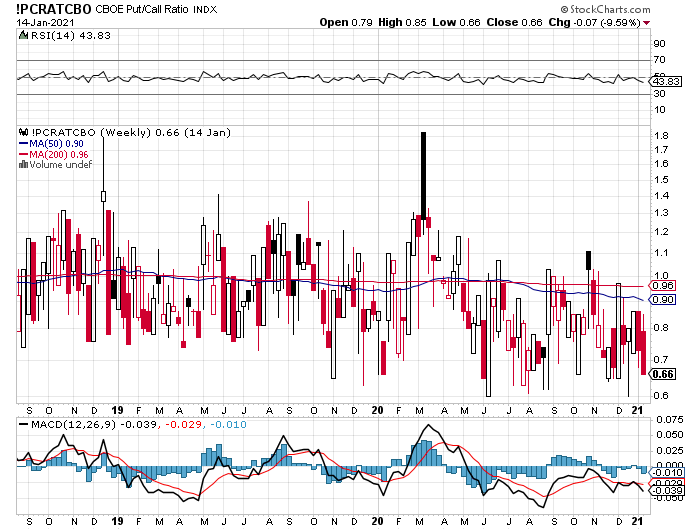

The Put/Call Ratio is currently low: 0.66 according to the chart below. That is as low as we have seen in the last 18 months (per the chart), and is in fact as low as it is been in the last 10 years. As it is a contrarian indicator, the Put/Call Ratio at the low 0.66 level is not a good sign for the near future. It means the stock market is currently over-bought.

Equity Put/Call Ratio (Weekly Chart) from Stockcharts.com

Meaning

Puts are options to sell stocks at a specific “strike” price and Calls are options to buy stocks at a specific “strike” price. Investors who buy Calls look for the underlying stock to go up, and Put buyers look for the stock to go down. Calls are optimistic plays, and Puts are pessimistic plays. When more Calls are purchased in aggregate than are Puts, the Put/Call ratio will be below 1, and vice versa. The ratio is normally slightly below 1 – the chart shows that its 200-day moving average is 0.96 – because stocks tend to go up more than down. Notice also in the chart that the Put/Call Ratio was about 1.8 back in March 2020, which is when we had our bear market correction as a result of the initial Coronavirus economic shutdown.

Contrarian

However, when the Put/Call Ratio moves more than 1 standard deviation from the mean, where it is now, it will likely mean revert back. That means the ratio will go up from its current 0.66, which means more puts will be bought than they are now, which means the stock market is likely headed lower in the near future until the ratio is more normalized.

IMO

It is a good idea to keep an eye on the Put/Call Ratio when you are trying to figure out if and when the market might reverse itself. Right now, it doesn’t look promising because the ratio is extremely low. Let’s see if it eases back to a more normalized number, or if the change is more drastic. Likely more drastic, if the past is any guide. Watch it!

After having read several economists’ reports regarding what they expect Federal tax policy will look like for 2021, I believe the most likely case is that any change in tax rates that Congress passes and President Biden signs will go into effect as of 1/1/22 and not retroactive to 1/1/21. Though there is a strong urge to purge anything and everything that the Trump administration did including tax cuts, I believe the remaining issues related to the economic troubles we face as a result of Covid will outweigh the urge to purge. Raising taxes during slow economic times is contrary to Keynesian orthodoxy and it makes no sense to raise taxes while at the same time writing checks directly to the citizenry. I believe you can count on current tax rates for individuals, corporations, and estates to remain as they currently are for 2021.

Better For Planning

If I am correct, then it would be really good for financial planners and/or anyone else who does their financial and tax planning for themselves. Uncertainty about tax laws and rates is bad because it makes planning difficult, even for a few months out. Conversely, if you know that rates are going to change as of next year and not retroactive to this year, you can make plans this year to address those changes. This goes for individuals, businesses, and estates. For instance, what if Congress doesn’t take up the tax debate until late in Q1 or even after that and doesn’t get it passed for a bit longer? If the law were to be retroactive back several months, then that would really be moving the goal posts well after the game has started. We need to be able to count on laws that are on the books at the start of the year remaining on the books for the entire year. Otherwise you have to change your entire attack in the middle of the game, and that is a recipe for disaster. Surely the new Congress and President recognize this, right?

Individual Tax Rates

For most of us, the rates that are most pertinent are Individual Tax Rates. The following are 2021 tax rates, taken from the IRS.gov website:

The tax items for tax year 2021 of greatest interest to most taxpayers include the following dollar amounts:

The standard deduction for married couples filing jointly for tax year 2021 rises to $25,100, up $300 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $12,550 for 2021, up $150, and for heads of households, the standard deduction will be $18,800 for tax year 2021, up $150.

The personal exemption for tax year 2021 remains at 0, as it was for 2020; this elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act.

Marginal Rates: For tax year 2021, the top tax rate remains 37% for individual single taxpayers with incomes greater than $523,600 ($628,300 for married couples filing jointly). The other rates are:

35%, for incomes over $209,425 ($418,850 for married couples filing jointly);

32% for incomes over $164,925 ($329,850 for married couples filing jointly);

24% for incomes over $86,375 ($172,750 for married couples filing jointly);

22% for incomes over $40,525 ($81,050 for married couples filing jointly);

12% for incomes over $9,950 ($19,900 for married couples filing jointly).

The lowest rate is 10% for incomes of single individuals with incomes of $9,950 or less ($19,900 for married couples filing jointly).

If in fact these rates remain the law through 2021, think about how you might use this standard deduction and these tax brackets to minimize your tax burden this year. Alternatively, perhaps use this information to pay taxes this year at a lower rate so that you don’t pay even higher taxes next year if and when the law changes. Hopefully soon you will have the proposed new tax laws and brackets to help you with that planning.

IMO

With the Democrats in power in DC and with astronomical budget deficits due to efforts to prop up the economy as a result of Covid, I think it is a pretty safe bet that taxes will be going up. However, I believe part of the recovery plan will be to keep them at their current lower rates this year, then raise them in 2022 when hopefully Covid will not be as much of a problem. Let’s see if I and the others who agree with me are correct.

Granted, it was an unusual year, but Growth investing outpaced Value investing in 2020 according to the metrics and definitions of both categories. The Center for Research of Security Prices (CRSP) publishes several stock indexes, two of which are the US Large Cap Growth Index and the US Large Cap Value Index. Whereas the Value Index was barely breakeven for 2020, the Growth Index returned about 33%. A big win for Growth Investing – or is it?

According To The Metrics and Definitions

Notice that I used the qualifying phrase “according to the metrics and definitions of both categories.” A Value Stock is considered as such and is included in a Value index if it meets one or more of certain “value” metrics such as low P/E ratio, low Price to Book or Price to Sales ratio, or low Price to Cash Flow ratio. A stock can be considered to be a value stock without being a good value. Conversely, a stock can be a good value (at least for some investors) even if doesn’t meet any of the value metrics. My point is that Value is in the eye of the beholder. You can invest in growth stocks and still consider yourself to be a “Value Investor” even if your investments don’t fit with the definition of value stocks. If you buy a stock with the belief that you are buying it at a price that is lower than what its value will be in the future, then you are a “Value Investor”. Consider this: One of Warren Buffett’s largest and best performing holdings is Apple. How can the most renowned value investor in the US own a big chunk of Apple, which is not a “value” company by any metric? Because Buffett believes in Apple’s ability to generate and grow its cash flow in the future, and that that cash flow discounted back to the present represents a positive net present value to Apple’s current stock price by his calculation. Buffett believes Apple’s current price represents good value to him and his shareholders even though Apple’s current ratios do not qualify it for any Value index.

IMO

If you are a committed value investor and your performance in 2020 has lagged, don’t give up being a value investor. Instead, enlarge the definition of what it means to be a value investor. Think about buying good companies at prices that make sense rather than finding unloved gems in the scrap heap. Good companies are rarely found at scrap heap prices. That said, they can often be found at prices that can be deemed to represent good investments if the future turns out the way you believe it will. This is not throwing in the towel on value investing. It is pivoting somewhat to allow you to keep in tune with market conditions while remaining faithful to Buffett’s and Benjamin Graham’s concepts of value investing.

Also: 2020 was one thing, but let’s see how 2021 plays out with respect to this supposed Value vs. Growth competition. My sense is that there won’t be nearly the difference in returns between the two categories.

Most New Year’s resolutions are pretty dull. Lose weight, exercise more, eat less, yadda yadda. Same with financial resolutions. Google it and see what comes up: create a budget, save more, spend less, work harder. Good advice all, but dull. With my 2021 Resolutions, I will try to be a little more interesting. Let’s see if I succeed.

Pay Cash

One of the selling points of Bitcoin is that you can use it to pay for stuff anonymously, leaving no digital footprint. Guess what else accomplishes the same objective? Good old cash! Don’t want anyone to know what you bought or how much you spent on it? Pay cash. Don’t like it when you get your credit card bill at the end of the month? Pay cash, and the stuff you bought won’t show up on your bill. I feel like I pay twice when I use the credit card – once when I buy the item, and again when I pay the credit card bill. Instead, just use cash and pay once. Go to the ATM once a week, withdraw as much cash as you need for the week, and when you have spent it all, that’s it until you go back to the ATM the next week. If you want to save for something big, stick a $20 in an envelope and put it in a drawer in your home. Do the same thing for 5 weeks and you have $100 you can use to treat yourself or your family. Buy your gasoline at an ARCO or another gas station that has a discount price for paying cash. It is becoming harder and harder to pay cash, especially with Amazon and electronic shopping, but that may make it more appealing. When you pay cash, you feel a little bit like you are getting away with something, and that is a good feeling that could prompt a wry smile.

Drink Cheap Liquor

My friend gave me a vodka drink with Sam’s Club store brand vodka, and it was really good. Same thing with Kirkwood-brand vodka from Costco, which rumor has it is actually Grey Goose in a different bottle. Two Buck Chuck from Trader Joes is pretty bad (imo), but some jug and box wines are actually pretty good. Try out some store brand liquor or wine and see what you think. Same thing with soda pop or seltzer water – try the much cheaper store brands. I’ve never been big on off-brand beer, but if you shop the specials at the store, you can shave several bucks off of the cost and enjoy the adventure if you aren’t too picky. All of you collectors of expensive wine have a nice hobby but not one that is good from a financial standpoint. You may tell yourself that it is, but it’s not if you are consuming a lot of high-end wine.

Figure Out A Way To Save On Phone, Internet, and Cable

Everyone has different options for phone, internet, and cable based mostly on where they live. Choose the option that best suits you and how you use these services. Make sure you get value for what you spend. For instance, many people have ditched their land line and have opted instead for an internet-based phone or just a cell phone. That doesn’t work well for our family because, for whatever reason, cell service in our house is spotty, and I am not a fan of the call quality of internet phones. So I still have a traditional land line with AT&T, but I called and downgraded the service and our bill is now only about 60% of what it was before. Those of you who are heavy internet users probably need a good, fast internet service, so you might use that as the starting point for what you pay for. Is your internet service reliable enough to stream you TV through it without degrading your ability to use the net? Then you might dump your cable TV service and go with a streaming TV service. All of the cable TV/internet providers have bundle services, and some of those bundles now include cell phone services. If you now have a stand-alone cell service, maybe you can save buy bundling up. Before you do, though, ask your neighbors if they have a different cell phone network provider than you do, and, if so, how well it works at home. Your objective should be to have quality service at a good price and not double-pay for some services. Take advantage of bundles if it makes sense with minimal sacrifice. This should be an annual exercise for you as the quality of some services change and technologies advance. For instance, as 5G service advances over the next few years, you may be able to ditch your expensive cable internet service entirely, which could realign a number of your spending priorities.

Deprioritize Politics

The TV pundits say we are a divided nation, but I think we are pretty united in our unhappiness with the current state of politics in the US. Unhappy perhaps for different reasons, but unhappy nonetheless. If watching the news on TV makes you unhappy, then don’t watch it. If your whole mood or attitude is based upon the political party in charge or what is happening in Washington DC or your state capitol, then you are setting yourself up for a life of anxiety and disappointment.

Prioritize Yoga

I don’t do yoga, but I like it, and I might take it up once the pandemic is over. Yoga is good for you physically and spiritually and hopefully puts you in a good state of mind. Unlike politics and watching the news. If not yoga, then some other physical activity such as just taking a walk or meditating or staring into space. Do some activity that puts you in a good state of mind and don’t let negative thoughts or activities ruin your life.

Buy Stocks Instead of Bonds

I say this because bond yields are so low, especially for US Treasury bonds and bank CDs. Stocks always outperform in the long run, and you can stay safe if you diversify your stock portfolio substantially. Instead of allocating to bonds, put like 1-2 years of your annual spending in a money market account in your bank, and invest the remainder in total market funds or ETFs.

Most people are happy that 2020 is coming to a close, and for several obvious reasons. Though I obviously didn’t enjoy all of the bad things that happened in 2020, I did enjoy how our country adapted and made the best of a bad situation. Our ability to adapt resulted in stock market indexes that are at or near all time highs despite all the bad that happened in 2020, and that is an accomplishment.

My Outlook for 2021

Interest rates are low and will continue to be low during 2021 and beyond. Rates may bump up a bit potentially at the longer end of the yield curve but you won’t make money investing in bonds during 2021. As a result, I think we need to re-think the “60/40” portfolio. Instead, investors should look to holding a certain amount of cash in their bank accounts, perhaps in a money market account, that they can access easily. Investors will earn almost as much in money market accounts as they will in other more sophisticated bond investments. If you can swing it, consider holding a year or more worth of your living expenses in a money market account. If you spend $200,000 per year, then put that into a money market. Call your bank or brokerage firm ahead of time to make sure you are getting the best money market rate that you can.

Invest The Rest

Once you have a sufficient cash reserve, then go ahead and invest the rest. I recommend a mixture of ETFs so that each investment you make is inherently diversified. Look at an S&P 500 Index ETF as the basis, and then potentially look at sector ETFs, including the tech-heavy Nasdaq 100 ETF. Consider emerging market or other international ETFs – there is an argument that the US dollar is headed lower, which will be good for international holdings. By investing in ETFs, including within fund families at firms such as Vanguard or Fidelity, you can diversify and still avoid paying high fees. Consider also dividend ETFs if you need current income, because your current return on dividend ETFs will be greater than the current return on bonds. I believe investors should overweight stocks as long as interest rates remain in the low range where they currently reside.

Geopolitical Issues

The coronavirus vaccine, continued economic recovery as a result of the vaccine, and the latest stimulus bill (depending on its final form) are all bullish for stocks. Stock indexes had a great run in 2020 especially after late March, but I believe the stock rally still has some legs. Internationally, Britain and the EU have reached a post-Brexit trade agreement, which will be good. Agreements between Israel and several Muslim countries are a good thing. Iran is becoming more and more isolated as a result of these agreements, so that remains as a threat, but there never is a time when there isn’t some kind of threat. I don’t see Iran striking out on its own without backing from other Muslim states. It will take all of 2021 to occur but the whole world will benefit from the coronavirus vaccine. Economies worldwide will recover, though likely at different rates. All of this will be bullish for economic activity and bullish for stocks.

Alternatives

Inflation hawks have been warning investors about looming inflation for years and it hasn’t happened yet. That said, deficit spending by governments worldwide is inflationary, if standard economics textbooks are to be believed. Will the trillions of dollars that governments have spent to keep their economies afloat finally cause the inflation predator to rear its ugly head? I believe inflation could be slightly higher but not significantly so. As a result, investors should slightly overweight their holdings of real assets such as gold, commodities, and especially residential real estate. Consider also Bitcoin, which is not a real asset but has been acting as an inflation hedge.

IMO

You may be wary of investing in stock indexes right when they are at or near highs, but consider what your investments might look like 3 to 5 years hence. Stocks may have their issues in the short term but have almost always outperformed in the long term. Don’t take any flyers on bubble stocks such as TSLA or hot IPOs such as DoorDash right now – wait and see how these shake out for a bit. If you miss some profits, oh well, but those profits will have been due to the greater fool theory rather than fundamental improvement. Stay diversified in stock ETFs and you should be rewarded during 2021.

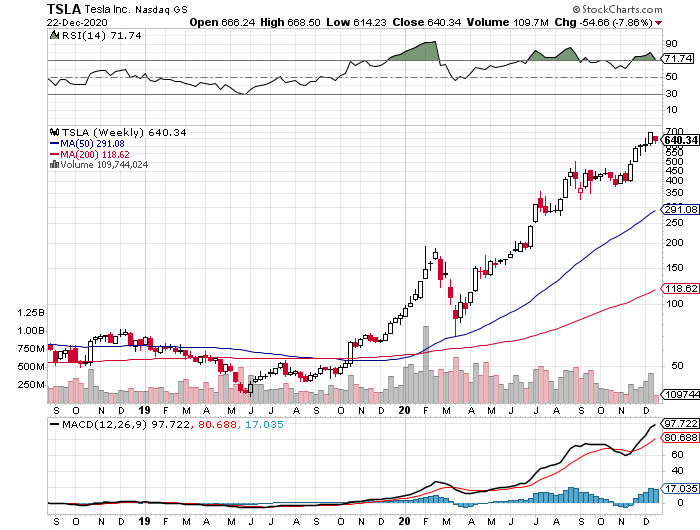

I have written a couple of posts before about Tesla. I thought it would have severe obstacles ahead of it especially as other car companies brought their own electric cars to the market. I thought it was overvalued prior to Covid. Now I think its recent performance is insane. There is no justification for TSLA to be the 6th or 7th (depending on how you view it) most valuable publicly-traded company, with a market cap of nearly $600 Billion, and worth more than the next 9 auto companies combined. Only if TSLA outperforms its most optimistic projections might this valuation make sense.

TSLA Weekly Chart from Stockcharts.com

Covid Is Bad For Cars

Why am I not a TSLA bull? For a number of reasons. Let’s start with the environment for new car sales. Covid and the resulting changes in the way we work can’t be good for future new car sales. People aren’t driving nearly as much. They are working from home so they are not driving to the office. Shopping opportunities are limited so they aren’t driving to go shopping. Families with multiple cars are considering whether they will continue to need multiple cars. The US population is getting older and retired couples are more likely not to have multiple cars. The China market is growing for Tesla so they do have that trend in their favor, but most other trends point to slowing car sales instead of increased sales. In looking for a catalyst to have propelled TSLA from under $100 in March 2020 to $640 today as I write this, I don’t see it in the potential growth in the new car market.

Move Toward Electric Cars

There is an argument that if a car buyer wants an electric car, they will want a Tesla and will likely not look at another brand of electric car. Other electric car brands have had real difficulty in catching on and sales projections have not been met. Tesla’s market share of the electric car market is over 80% in the US, but Tesla is less than 2% of the new car market inclusive of gasoline cars. So, if Tesla retains its 80% EV market share and is able to grow its overall market share to 10%, then perhaps you have an argument for growth, but not to the extent that TSLA has already performed. Governor Newsom’s recent mandate that 100% of all car sales in 2035 in California must be zero emission vehicles points toward an increase in EV sales, but we will see how well Newsom’s mandate will be enacted, especially since it was a mandate and not a law and since he will likely be gone from the scene by 2035.

S&P 500

Now TSLA has been moved into the S&P 500 Index. However, guess what? TSLA has underperformed in the days since it has been added to that Index. Perhaps the buy-up occurred prior to the actual inclusion on the Index, and investors will dump TSLA now that its inclusion is complete. We will see, but perhaps this is an instance of buy on the rumor and sell on the news.

A Bubble

I can view TSLA’s 2020 performance only as a bubble propelled by major money chasing momentum plays. There has been no catalyst resulting from Covid or from anywhere else in 2020 that has caused TSLA to be fundamentally worth nearly $600 Billion. There are no traditional metrics that make sense. Perhaps I am showing my age here but if you are long TSLA here you are risking a lot. Jump off now before everyone else does.

There are a number of reasons why you should strongly consider converting part or all of your traditional IRA or 401k accounts into a Roth IRA. The Covid shutdown economy this year adds to the list.

Here are some the reasons to do a Roth Conversion:

If your investment portfolio is in a loss position this year, any tax hit you incur as a result of the Roth conversion would be offset by the investment losses. This looked like an appealing aspect of the weak stock market earlier this year but as the year has gone on and the markets have recovered, there probably aren’t as many investment losses to be taken advantage of.

If you have been laid off or your Adjusted Gross Income for 2020 will otherwise be lower than expected, then perhaps the income that you book by doing a Roth conversion may not hurt you as much this year and may not cause your taxes to increase substantially. You can “take advantage” of this off year in your own income by paying taxes now on your traditional retirement fund cash and thereby minimize taxes you might have to pay at a later date during your retirement.

Speaking of which, you might have read that there will be a new President next year. As a result of the new administration, and as a result of the explosion in government spending in 2020 in an effort to keep the economy together as a result of the coronavirus economy, do you believe your taxes going forward are more likely to go up or go down? If you agree that taxes are more likely to go up, then it is advantageous for you to convert your IRA to a Roth now rather than later at a higher tax rate.

Roth IRAs have no Required Minimum Distributions and are not taxable to the owner if the owner has held the Roth account for at least 5 years. (Roth 401k’s do have RMD requirements). Compare that with traditional IRA and 401k accounts, which are taxable as ordinary income and which have strict RMD requirements. Though it is more painful (tax-wise) to do a Roth at the front end, the Roth is much better at the withdrawal end.

You don’t have to convert 100% of your traditional retirement account at once. You can stage your conversion over a number of years, or just convert a part of it and leave the rest alone.

If you are over 59 1/2 years old, you don’t have to pay the 10% penalty on the portion that you convert – just ordinary income on that part.

You don’t have to pay the IRS from your traditional retirement account money. In other words, whatever your traditional retirement account balance is pre-conversion, it can be the same balance after you convert it to a Roth, as long as you have enough money elsewhere to pay the additional taxes you incur by doing the conversion. Keep in mind, converting a traditional retirement to a Roth IRA is equivalent (from a tax perspective) to withdrawing the money from the traditional account, meaning it is treated as ordinary income to you.

Do some analysis prior to converting. Look at the Federal and State (if appropriate) tax tables. If, by doing a conversion, you force yourself into a significantly higher tax bracket, then don’t convert, or convert a smaller amount.

Unlike setting up or contributing directly to a Roth IRA, there are no income limits on doing a Roth conversion. This “backdoor” way of having a Roth IRA is explicitly legal because it raises more money for the IRS in the short term.

IMO

If you are heading into retirement, and especially if you are over 59 1/2 years old, you should certainly analyze and strongly consider doing a Roth conversion. I am afraid that taxes will have to be raised significantly in order to pay for what government has had to do to keep the economy from imploding this year. Any tax money you can spend now that saves you from spending money when you need it in retirement is a good idea.

“It’s always darkest before the dawn” was most recently uttered in pop culture by Florence and the Machine. With the coronavirus vaccine now approved and in initial distribution now at the same time as coronavirus infections and hospitalizations at an all time high in the US, it seems we have a “darkest before the dawn” situation now. How do you think the new vaccine will affect the US and World economies in 2021 and beyond? Without a doubt the effect will be good, but how good? And what does it mean for your financial goals?

For Fixed Income

If you agree that the vaccine will be a good thing and that economic output and metrics will improve as a result, that is not good for fixed income. Improved economic output likely means higher interest rates which means lower bond prices. Because the US Fed has indicated it will keep short-term interest rates low for likely the next 2 years, look for longer-term interest rates to rise and therefore look for the yield curve to steepen. With the 10-Year US Treasury rate currently at about 90 basis points, look for it to move to between 2% and 2.5% by 12 months from now. Are you busy now refinancing your house? Good idea, because mortgage rates should also be up by a similar 120 basis points or more in a year. Investment grade corporate bonds, currently in the low-2% range, should be in the high 3%’s, which isn’t a big stretch because that’s where they were during early 2019. My recommendation is to underweight fixed income and to stay short-term on what fixed income you do have. If you are a borrower (i.e. mortgate) then its a great idea to lock in now for the long term. If you are a lender (i.e. fixed income investor), then not such a good idea to lock in now.

For Alternatives

This to me is the biggest question mark. Will inflation return or not, and if so how much? While there is debate now as to whether or not Gold is an inflation hedge, historically it has been considered as such. If you buy that argument, then investors seem to be hedging their bets as to how inflationary the fiscal and especially the monetary policy reactions to the pandemic economy will turn out to be. Oil has been rallying for the past 2 months and copper and lumber have also been strong, all of which indicate stronger future economic activity and as well higher inflation. All that said, inflation hawks have been out there before and have been wrong in the past. I think a balanced portfolio should have some exposure to inflation-leveraged assets and an investor should slightly overweight their exposure in this area. Perhaps look at inflation-protected TIPS, or Google “Inflation ETF” and read about ETFs that are inflation-protected. If you own real estate, either in your home or through a rental property, then you may consider that you are already properly positioned against the inflation threat. Bitcoin? It has been very strong but I’m not sure Bitcoin’s strength has been a reaction to higher inflation or a reaction to a concern about the ability of world governments to survive and to continue to govern post-pandemic.

Equities

The vaccine is bullish for equities. However, has the run-up we have had in equities since late March 2020 already captured the upside reflective of the improved post-pandemic economy? Said another way, is the upside already priced in at current equity prices? I don’t believe so, and I do believe there is more upside to be had by being invested in equities. My reasoning is the TINA argument – there is no alternative. Because I see interest going up especially at the longer end and with mortgages and corporate bonds, I see investors moving out of the fixed income sector and increasing their exposure in the equities space. Corporate earnings, especially among the biggest companies and including the FAANG stocks, should be strong and should continue to improve. I believe investors should overweight equities. Though their returns may or may not be in the double-digits, they will likely exceed what they might earn in fixed income.

IMO

Even though the run-up in equities since March has been strong, I believe the rally has more legs. I also see longer term interest rates going up and therefore I believe investors should overweight equities. Look also to invest such that you might benefit from higher inflation. Refinance your mortgage now if you are looking to do so and haven’t already done so. With the coronavirus vaccine now at the very start of being administered, let’s hope that the vaccine rollout works, not just for our portfolios but for all of humanity.

DoorDash IPO’d Wednesday and it was a smashing success. Not only did DoorDash price its IPO 13% higher than they had forecast and raising about a half a $ Billion more than they thought they would, but the stock then rose by 86% once it went public. Its close at $189 and change meant that its market cap was $72 Billion at the close on Wednesday, or about the same as Colgate-Palmolive and larger than General Motors. Outstanding for a company whose business is transporting hot food that they don’t cook themselves to your front door.

Too High?

Does it stretch reality to consider that a food delivery company is worth more than GM? This article from Yahoo Finance makes the bearish case. DoorDash lost $667 Million in 2019 and posted a loss of $149 Million through the first 3 quarters of 2020 even though the environment for its service was in full sail due to the pandemic. Will the advent of the vaccine mean the downwind gust will ebb and become more of a gentle breeze? Will a vaccinated population quickly revert back to its pre-pandemic ways and go back out to restaurants en masse? Or will a sizeable portion of pre-pandemic restaurant patrons stay at home, if not permanently than at least more often than they used to? And, if so, will it be enough such that DoorDash can become profitable? It’s hard to envision how and when DoorDash will turn a profit if they can’t do so in 2020.

Not High Enough?

The food delivery market is fragmented among DoorDash, UberEats, Postmates, GrubHub, and a number of smaller players. The Yahoo Finance article sees this market fragmentation as problematic, but it could be an opportunity for a well-capitalized DoorDash to snap up market share by acquiring smaller players. DoorDash bought smaller competitor Caviar last year and now has a 45% market share in home food delivery according to this article.

Another opportunity for DoorDash is that the percentage of people who order home food delivery is still relatively small – somewhere between 6% and 20%, and probably around 10%. Some customers prefer to pick up their food themselves, and some restaurants have their own delivery services rather than farm out the task to a third party like DoorDash. If DoorDash performs, perhaps it can grow its own market.

IMO

All new tech IPO’s have their skeptics. I believe there is a good and growing market for food delivery in the US and my own experiences with DoorDash have been good: the food arrives on time and hot. That said, the current valuation reflects the most optimistic of sales and profit projections. A number of recent IPO’s, including Uber and Lyft, followed a pattern of a strong IPO followed by poor subsequent performance for several quarters, followed by strength as the economy recovers from the pandemic lockdowns. Look for a similar pattern for DoorDash: several quarters as the business matures and DoorDash’s performance catches up with these lofty initial projections. Don’t buy now but watch to see how DoorDash and the home food delivery market plays out.

Perhaps you read last week that Salesforce is buying Slack for over $27 Billion. That’s nice, but why should you care? Because the acquisition (assuming it is completed) is another step in the direction of employers allowing their employees to work remotely including from home. It helps to solidify this work from home economy that was spawned by the pandemic. The ramifications on the work from home economy are significant and could be fatal to ancillary businesses related to the “traditional” office workplace.

Slack

Slack’s main software product allows employees of the same company to communicate with one another in a better way. It advertises itself as a replacement for traditional email, but Slack is much more than that. In addition to video calling, Slack allows workers to work together by sharing documents such as spreadsheets or slides so that they can work collaboratively on a project. Rather than sitting in a conference room at the office, workers using Slack can be anywhere that has good internet access and meet together with people on their team to hash out a set of slides that they need to complete in preparation for an important meeting. This type of Slack-enabled workforce collaboration is how the US economy didn’t totally collapse during the pandemic and the various shutdowns and it is how the economy (per GDP figures) has recovered as strongly and as quickly as it has.

Salesforce

Salesforce’s main product is customer relationship management software, so much so that its stock exchange ticker symbol is CRM. Since the focus of Salesforce’s software tracks the order and sales process between companies and is thus more of a business to business product. Slack, therefore, does not compete with Salesforce’s current software but there should be some synergies insofar as Salesforce’s current customers could also be potential Slack customers if they aren’t already. What Salesforce brings to Slack are more resources: money, people, and an existing customer base. Slack could grow its sales substantially more as part of Salesforce than they could as a stand alone company because Salesforce has more money to put toward sales growth.

Microsoft Teams

Slack competes directly with Microsoft Teams and it isn’t a fair fight because Teams is included in the Microsoft Office package whereas Slack is a stand alone product from a stand alone company. Slack’s advantage is that it is considered to be superior to Teams but they can’t compete with the behemoth Microsoft. Enter Salesforce, which though it is not on the level of Microsoft is much bigger than Slack ($200 Billion market cap vs. $27 Billion). Now Slack will at least have a fighting chance of staying in the ring in its battle with Teams for the market for collaborative office working software.

Why This Matters

This matters because now, with Teams and a bulked-up Slack battling for the market, it means that more companies will get comfortable with the idea that their employees can be productive working from home and that the trend will grow. What does that mean for landlords who own office buildings, especially Class B or C buildings? What does it mean for vendors who cater to the downtown office worker lunch business? It can’t be good for downtown ancillary businesses. Don’t look to load up on the stocks of office REITs. On the other hand, if you live (and now work) in the ‘burbs, this work from home trend could be good for local neighborhood retailers, especially once the vaccine is administered yet people are still working from home. What about the price of oil, and hence the stock of oil producers? If people aren’t driving to work, then they aren’t buying gas. If they aren’t buying gas, then maybe they don’t need their own car, and maybe they can share a car. That’s not good for the auto makers. However, if your work from home situation leaves something to be desired, perhaps you are looking to upgrade your existing abode or maybe buy a new one. That speaks well for home builders as well as the Home Depots of the world, especially if mortgage rates remain low, as is expected.

IMO

I am not saying that Salesforce’s acquisition of Slack is going to cause the office market to collapse along with General Motors. I am saying that the proposed transaction is a sign that indicates that work from home is a trend that will remain in place even after everyone is vaccinated from Covid. Don’t go bargain hunting right now for stocks tied to a return to the work at the office economy because even though it may look like a bargain now, it could look even worse a year from now.